Medicare Part D

What Will Medicare Part D Cost Sharing Look Like in 2025?

Starting January 1, 2025, the Medicare Part D coverage gap—commonly referred to as the “donut hole”—will no longer exist. This significant update, brought about by the Inflation Reduction Act, simplifies prescription drug coverage and introduces a $2,000 annual cap on out-of-pocket expenses for covered medications.

The following phases outline how out-of-pocket costs are managed under Part D throughout the year:

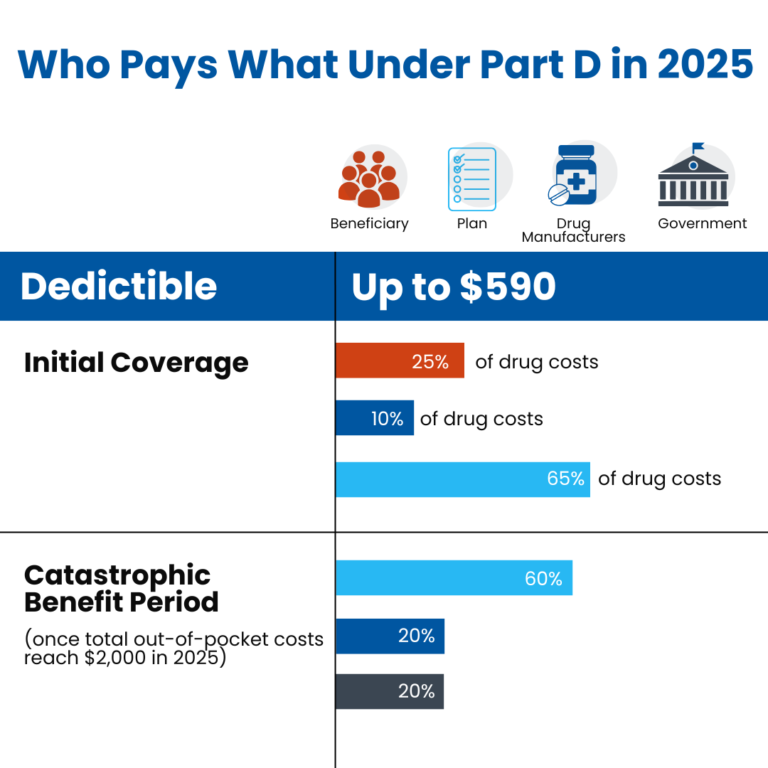

♦ Deductible Phase: During this initial stage, beneficiaries are responsible for paying 100% of their prescription drug costs until they meet the deductible amount. For 2025, the standard deductible is set at $590. However, certain plans may feature a lower or even zero-dollar deductible paired with a higher premium. Once the deductible is satisfied, beneficiaries move into the initial coverage phase.

♦ Initial Coverage Phase: In this stage, beneficiaries are required to cover 25% of their prescription drug expenses, typically through coinsurance or copayments. The Part D plan contributes 65% of the costs, and drug manufacturers account for the remaining 10%. Out-of-pocket spending, including deductibles, copayments, and coinsurance, is capped at $2,000 for 2025. Upon reaching this limit, beneficiaries transition to catastrophic coverage.

♦ Catastrophic Coverage Phase: At this level, the Part D plan covers 60% of drug costs, the manufacturer covers 20%, and Medicare handles the remaining 20%. Beneficiaries are no longer responsible for any additional payments for covered prescriptions for the rest of the year.

For a clearer understanding, our infographic below illustrates the cost-sharing responsibilities within the different phases of Medicare Part D coverage in 2025.